> ## Documentation Index

> Fetch the complete documentation index at: https://v3.docs.derive.xyz/llms.txt

> Use this file to discover all available pages before exploring further.

# Managers & Risk Universes

> How margin managers and risk universes shape what a subaccount can trade and hold.

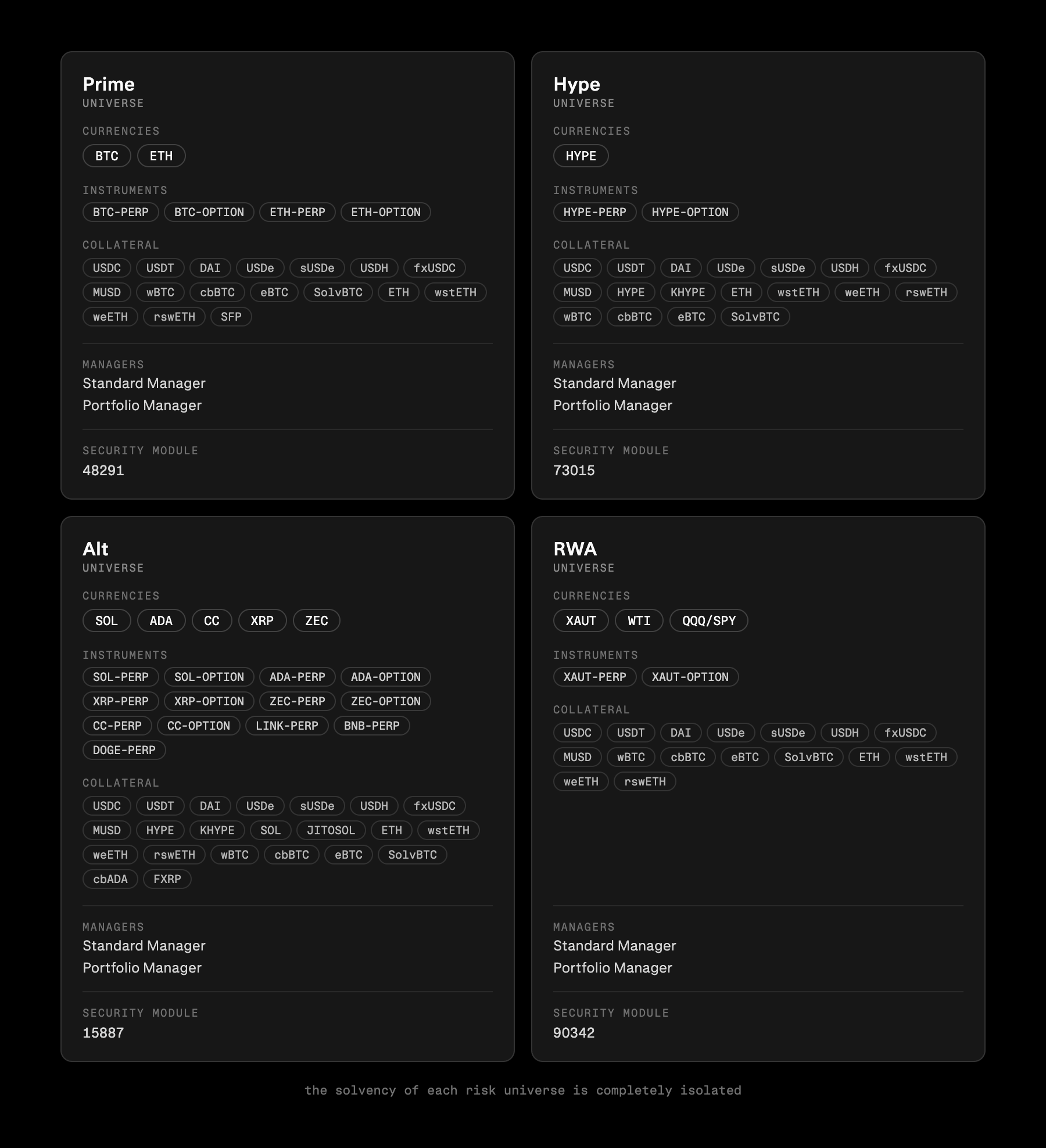

Every subaccount is bound to a **manager** and, through it, to a **risk universe**. Together they

decide the margin model you get, which instruments you can trade, and which assets you can post as

collateral. You never set the universe directly — you pick a `manager_id`, and everything else

follows.

The margin model applied to your subaccount — **Standard** (cross collateral margin) or

**Portfolio** (scenario-based netting). You choose one via `manager_id` at subaccount creation.

A risk-containment boundary. A universe's collateral, open-interest, and lending rules are its

own, and losses are socialized only **within** it — so trades never cross universes.

## How they relate

* A subaccount can only have **one** manager.

* A manager belongs to **exactly one** universe.

* A universe exposes **at most one Standard and one Portfolio** manager.

* You choose a `manager_id`; that fixes both your **margin model** and your **universe**.

See the `public/get_all_currencies` section below to get the latest breakdown of managers and risk universes.

## Managers

A manager is the margin engine that risk-prices your subaccount. There are two:

| Manager | Wire label | Margin model | Best for |

| ------------- | ---------- | -------------------------------------------------------------------------------- | ------------------------------------------------------------------- |

| **Standard** | `SM` | Cross-collateral: collaterals contribute margin but options margined separately. | Simple/directional positions and collateral-style holding. |

| **Portfolio** | `PM2` | Scenario-based: a whole book netted across a grid of shocks. | Complex option/perp books that benefit from cross-position offsets. |

Each manager has a numeric **`manager_id`**. A subaccount stores its `manager_id` and derives its

universe, tradeable instruments, and accepted collateral from it. Picking Standard vs Portfolio for

the same book changes your margin requirement, not what you can hold.

## Risk universes

A risk universe is a set of assets and managers that share a single risk boundary. It exists so

that an insolvency in one universe can only ever be absorbed by that universe's own Security Module

and, if needed, socialized to solvent accounts **inside the same universe** — never across the

whole exchange. As a direct consequence, **a trade, RFQ, or liquidation is rejected if the two

sides sit in different universes.**

Everything risk-related is keyed by `(asset, risk_universe_id)`: collateral discounts, OI caps, and

lending pools can all differ per universe for the very same asset.

## The fallback universe

Universe **`0`** is a special **fallback** ("lost-and-found") universe: a no-margin holding area whose

only job is to safely custody collateral that has nowhere else to go. It registers every spot asset

but supports **no trading, borrowing, options, or perps**.

Every wallet is given a single fallback subaccount when its account is created. A deposit lands there —

instead of the subaccount you intended — whenever it can't be honoured as requested:

* it targets the fallback manager (`manager_id` `0`),

* the asset isn't registered in the target manager's universe, or

* the amount is below the subaccount-creation fee.

Funds in the fallback subaccount are safe but idle — you can't trade against them. To put them to work,

move the spot out to a real subaccount with `private/transfer_spot`.

## Reading `public/get_all_currencies`

`public/get_all_currencies` (no params; `public/get_currency` for a single one) is the source of

truth for **what is supported where**. Each currency lists its managers per universe and its assets'

risk per universe, so a single response tells you which `manager_id` to use and what you can trade

or post against it.

```json Response (abridged, one currency) theme={null}

{

"currency": "ETH",

"market_type": "ALL",

"spot_price": "1950.0",

"managers": [

{ "risk_universe_id": 1, "sm": 3, "pm": 12 }

],

"option": {

"name": "ETH-OPTION",

"address": "0x…",

"universes": [ { "risk_universe_id": 1, "oi": { "current_open_interest": "…", "interest_cap": "…" } } ]

},

"perp": {

"name": "ETH-PERP",

"address": "0x…",

"universes": [ { "risk_universe_id": 1, "oi": { "current_open_interest": "…", "interest_cap": "…" } } ]

},

"spot": [

{

"name": "ETH",

"address": "0x…",

"erc20": { "decimals": 18, "underlying_erc20": "0x…" },

"min_deposit_usd": "…",

"universes": [

{

"risk_universe_id": 1,

"srm_im_discount": "0.8",

"srm_mm_discount": "0.9",

"pm2_im_discount": "0.85",

"pm2_mm_discount": "0.92",

"lending": { "borrow_apy": "…", "supply_apy": "…", "total_borrow": "…", "total_borrow_cap": "…" },

"oi": { "current_open_interest": "…", "interest_cap": "…" }

}

]

}

]

}

```

Everything hangs off `risk_universe_id` — match it across `managers[]`, `option`/`perp.universes[]`,

and `spot[].universes[]` to read one universe consistently.

| To determine… | Read… |

| ----------------------------------------------------------------- | -------------------------------------------------------------------------------------------------------------------------------- |

| Which universes cover the currency, and which `manager_id` to use | `managers[]` → `{ risk_universe_id, sm, pm }` (`sm` = Standard id, `pm` = Portfolio id; either may be absent) |

| Whether options / perps exist for it | presence of top-level `option` / `perp`; their `universes[].oi` gives per-universe open interest and cap |

| Whether a spot asset is accepted as **collateral** | `spot[].universes[]` for your universe: `srm_im_discount` (Standard) / `pm2_im_discount` (Portfolio). `"0"` = not accepted there |

| Whether you can **lend / borrow** it | `spot[].universes[].lending` — `null` means no pool in that universe; otherwise APYs + `total_borrow_cap` |

| Remaining OI / supply headroom | `*.universes[].oi.{current_open_interest, interest_cap}` and `lending.{total_borrow, total_borrow_cap}` |

| Which classes are enabled at a glance | `market_type` (see below) |

`market_type` is a quick summary of the enabled classes; the authoritative check is which of

`option` / `perp` / `spot` are actually populated.

| `market_type` | Enabled classes |

| ----------------- | --------------------------------------------------- |

| `ALL` | Options, perps, and spot/collateral. |

| `SRM_OPTION_ONLY` | Options only. |

| `SRM_PERP_ONLY` | Perps only. |

| `SRM_BASE_ONLY` | Usable only as Standard-manager base collateral. |

| `CASH` | Cash/quote collateral only (e.g. a USD stablecoin). |

A currency can register several spot assets — e.g. a lending `USDC` and a non-lending `USDC-NL`. They appear as

separate entries in `spot[]` with their own discounts and lending, so check the specific `name`/`address` you intend

to deposit.

### Picking your manager

Find the currency and the `risk_universe_id` you want to trade in (typically the main universe, `1`).

From that universe's `managers[]` entry, use `sm` for Standard (isolated) margin or `pm` for Portfolio margin.

Check the asset you plan to post has a non-zero `srm_im_discount` (for `sm`) or `pm2_im_discount` (for `pm`) in the

same universe. `"0"` means that manager won't count it as collateral.

Pass the chosen id as `manager_id` when depositing to a new subaccount (see [Depositing](/getting-started/depositing)). Universe,

instruments, and collateral set all follow from it. You can read them back on

`private/get_subaccount` via its `manager_id` and `risk_universe_id`.

Choosing the wrong id has consequences at deposit and trade time:

* **Fallback routing** — depositing to a new subaccount under the fallback manager (`0`), an asset the universe

doesn't register, or below the creation fee lands the funds in your no-margin **fallback subaccount**, where they

can't be traded.

* **Cross-universe trade** — a subaccount can't trade against a counterparty in a different universe; the order is

rejected.

* **Wrong margin model** — Standard margins each position in isolation; picking it when your book needs cross-position

netting means a much higher requirement for the same positions.

## Related topics

- [Programmatic Onboarding](/getting-started/depositing.md)

- [New features](/migrating/new-features.md)

- [Error Codes](/error-codes.md)

See the `public/get_all_currencies` section below to get the latest breakdown of managers and risk universes.

## Managers

A manager is the margin engine that risk-prices your subaccount. There are two:

| Manager | Wire label | Margin model | Best for |

| ------------- | ---------- | -------------------------------------------------------------------------------- | ------------------------------------------------------------------- |

| **Standard** | `SM` | Cross-collateral: collaterals contribute margin but options margined separately. | Simple/directional positions and collateral-style holding. |

| **Portfolio** | `PM2` | Scenario-based: a whole book netted across a grid of shocks. | Complex option/perp books that benefit from cross-position offsets. |

Each manager has a numeric **`manager_id`**. A subaccount stores its `manager_id` and derives its

universe, tradeable instruments, and accepted collateral from it. Picking Standard vs Portfolio for

the same book changes your margin requirement, not what you can hold.

## Risk universes

A risk universe is a set of assets and managers that share a single risk boundary. It exists so

that an insolvency in one universe can only ever be absorbed by that universe's own Security Module

and, if needed, socialized to solvent accounts **inside the same universe** — never across the

whole exchange. As a direct consequence, **a trade, RFQ, or liquidation is rejected if the two

sides sit in different universes.**

Everything risk-related is keyed by `(asset, risk_universe_id)`: collateral discounts, OI caps, and

lending pools can all differ per universe for the very same asset.

## The fallback universe

Universe **`0`** is a special **fallback** ("lost-and-found") universe: a no-margin holding area whose

only job is to safely custody collateral that has nowhere else to go. It registers every spot asset

but supports **no trading, borrowing, options, or perps**.

Every wallet is given a single fallback subaccount when its account is created. A deposit lands there —

instead of the subaccount you intended — whenever it can't be honoured as requested:

* it targets the fallback manager (`manager_id` `0`),

* the asset isn't registered in the target manager's universe, or

* the amount is below the subaccount-creation fee.

Funds in the fallback subaccount are safe but idle — you can't trade against them. To put them to work,

move the spot out to a real subaccount with `private/transfer_spot`.

## Reading `public/get_all_currencies`

`public/get_all_currencies` (no params; `public/get_currency` for a single one) is the source of

truth for **what is supported where**. Each currency lists its managers per universe and its assets'

risk per universe, so a single response tells you which `manager_id` to use and what you can trade

or post against it.

```json Response (abridged, one currency) theme={null}

{

"currency": "ETH",

"market_type": "ALL",

"spot_price": "1950.0",

"managers": [

{ "risk_universe_id": 1, "sm": 3, "pm": 12 }

],

"option": {

"name": "ETH-OPTION",

"address": "0x…",

"universes": [ { "risk_universe_id": 1, "oi": { "current_open_interest": "…", "interest_cap": "…" } } ]

},

"perp": {

"name": "ETH-PERP",

"address": "0x…",

"universes": [ { "risk_universe_id": 1, "oi": { "current_open_interest": "…", "interest_cap": "…" } } ]

},

"spot": [

{

"name": "ETH",

"address": "0x…",

"erc20": { "decimals": 18, "underlying_erc20": "0x…" },

"min_deposit_usd": "…",

"universes": [

{

"risk_universe_id": 1,

"srm_im_discount": "0.8",

"srm_mm_discount": "0.9",

"pm2_im_discount": "0.85",

"pm2_mm_discount": "0.92",

"lending": { "borrow_apy": "…", "supply_apy": "…", "total_borrow": "…", "total_borrow_cap": "…" },

"oi": { "current_open_interest": "…", "interest_cap": "…" }

}

]

}

]

}

```

Everything hangs off `risk_universe_id` — match it across `managers[]`, `option`/`perp.universes[]`,

and `spot[].universes[]` to read one universe consistently.

| To determine… | Read… |

| ----------------------------------------------------------------- | -------------------------------------------------------------------------------------------------------------------------------- |

| Which universes cover the currency, and which `manager_id` to use | `managers[]` → `{ risk_universe_id, sm, pm }` (`sm` = Standard id, `pm` = Portfolio id; either may be absent) |

| Whether options / perps exist for it | presence of top-level `option` / `perp`; their `universes[].oi` gives per-universe open interest and cap |

| Whether a spot asset is accepted as **collateral** | `spot[].universes[]` for your universe: `srm_im_discount` (Standard) / `pm2_im_discount` (Portfolio). `"0"` = not accepted there |

| Whether you can **lend / borrow** it | `spot[].universes[].lending` — `null` means no pool in that universe; otherwise APYs + `total_borrow_cap` |

| Remaining OI / supply headroom | `*.universes[].oi.{current_open_interest, interest_cap}` and `lending.{total_borrow, total_borrow_cap}` |

| Which classes are enabled at a glance | `market_type` (see below) |

`market_type` is a quick summary of the enabled classes; the authoritative check is which of

`option` / `perp` / `spot` are actually populated.

| `market_type` | Enabled classes |

| ----------------- | --------------------------------------------------- |

| `ALL` | Options, perps, and spot/collateral. |

| `SRM_OPTION_ONLY` | Options only. |

| `SRM_PERP_ONLY` | Perps only. |

| `SRM_BASE_ONLY` | Usable only as Standard-manager base collateral. |

| `CASH` | Cash/quote collateral only (e.g. a USD stablecoin). |

A currency can register several spot assets — e.g. a lending `USDC` and a non-lending `USDC-NL`. They appear as

separate entries in `spot[]` with their own discounts and lending, so check the specific `name`/`address` you intend

to deposit.

### Picking your manager

Find the currency and the `risk_universe_id` you want to trade in (typically the main universe, `1`).

From that universe's `managers[]` entry, use `sm` for Standard (isolated) margin or `pm` for Portfolio margin.

Check the asset you plan to post has a non-zero `srm_im_discount` (for `sm`) or `pm2_im_discount` (for `pm`) in the

same universe. `"0"` means that manager won't count it as collateral.

Pass the chosen id as `manager_id` when depositing to a new subaccount (see [Depositing](/getting-started/depositing)). Universe,

instruments, and collateral set all follow from it. You can read them back on

`private/get_subaccount` via its `manager_id` and `risk_universe_id`.

Choosing the wrong id has consequences at deposit and trade time:

* **Fallback routing** — depositing to a new subaccount under the fallback manager (`0`), an asset the universe

doesn't register, or below the creation fee lands the funds in your no-margin **fallback subaccount**, where they

can't be traded.

* **Cross-universe trade** — a subaccount can't trade against a counterparty in a different universe; the order is

rejected.

* **Wrong margin model** — Standard margins each position in isolation; picking it when your book needs cross-position

netting means a much higher requirement for the same positions.

## Related topics

- [Programmatic Onboarding](/getting-started/depositing.md)

- [New features](/migrating/new-features.md)

- [Error Codes](/error-codes.md)